Passive Funds Don't Negotiate

- bespoke62

- 23 hours ago

- 5 min read

Three private companies with a combined value approaching $3.5 trillion are moving closer to public listings: SpaceX, OpenAI and Anthropic. This represents a rare clustering of very large initial public offerings in two of the most talked-about sectors of the decade: artificial intelligence and private space exploration. An initial public offering, or IPO, is when a private company lists on a stock exchange and its shares become publicly tradable.

The most important point for investors is not about the opportunities or technologies involved. It is about what happens when companies of this size list, and how index funds are required to respond.

An index is a collection of equity shares in companies listed across various markets, such as the NASDAQ in the US, or the FTSE in the UK. An index or passive fund is a fund which invests by mirroring these indices. These funds don't choose what they own. When a company joins an index, every fund that tracks that index must buy it. The purchase happens at whatever price the market is charging at the time, whether that price is low, fair, or expensive. Passive funds do not assess whether a share represents good value before buying it; they simply buy it when it enters the index.

This can also create what some investors call a "passive tax": passive investors often only gain exposure to a company once it has become large enough to be included in an index. As a result, they may miss much of the company's earlier growth while it was still privately owned, with early investors and insiders capturing much of that value creation.

As of June 2026, the potential listings of SpaceX, OpenAI and Anthropic have moved from a distant possibility to a realistic prospect over the next year. Timelines may still shift, and not every listing is guaranteed. Even so, the window is now close enough to think about the implications.

The headlines will likely frame these IPOs as "democratising access" to the future of AI and space. The reality for index investors is less about access and more about timing and price.

Why are these companies considering listing now?

Two forces are pushing these companies towards public markets. First, the era of near-zero interest rates that allowed private companies to raise huge sums and stay private has ended; venture backers want their money back. Second, public markets are currently very receptive to AI and space businesses. Investor enthusiasm is high, valuations are generous, and companies generally prefer to list when market conditions are most favourable, as it allows them to raise capital very cheaply from investors who are willing to pay.

The broader market reflects this optimism. The S&P 500 is trading at a price-to-earnings (PE) ratio of 29x, over 30% more expensive than its 30-year average. Investors are paying high prices today for high growth that is expected in the future.

If AI and commercial space activities genuinely turn out to be general-purpose technologies that reshape entire economies, today's prices may eventually look modest. A public listing also funds the land-grab phase, where early leaders can pull far ahead. We are not arguing that the optimistic view is wrong, only that paying a high price for a good idea can still produce a poor return. Cisco was one of the defining technology companies of its era, yet investors who bought at the height of the dotcom boom spent many years waiting to recover their money.

Passive funds are a guaranteed buyer of large IPOs

When a private company lists, it rarely sells the whole business. A typical IPO might only offer a small portion of shares to the public at first, often around 10–15%. This portion is known as the free float. The remaining 85–90% stays with founders, employees and early investors and cannot usually be sold for several months. A small float creates artificial scarcity. Lots of buyers chasing a limited supply of shares pushes the price higher. In addition, companies selling the future – as in the case of our three candidates – have a tendency to be very bullish on their prospects. This is when index funds are required to buy, while the number of tradable shares remains limited, when news flow is positive, and before additional supply comes to market. In the AI race, OpenAI and Anthropic have the opportunity to scale up via public market capital before others are fully established.

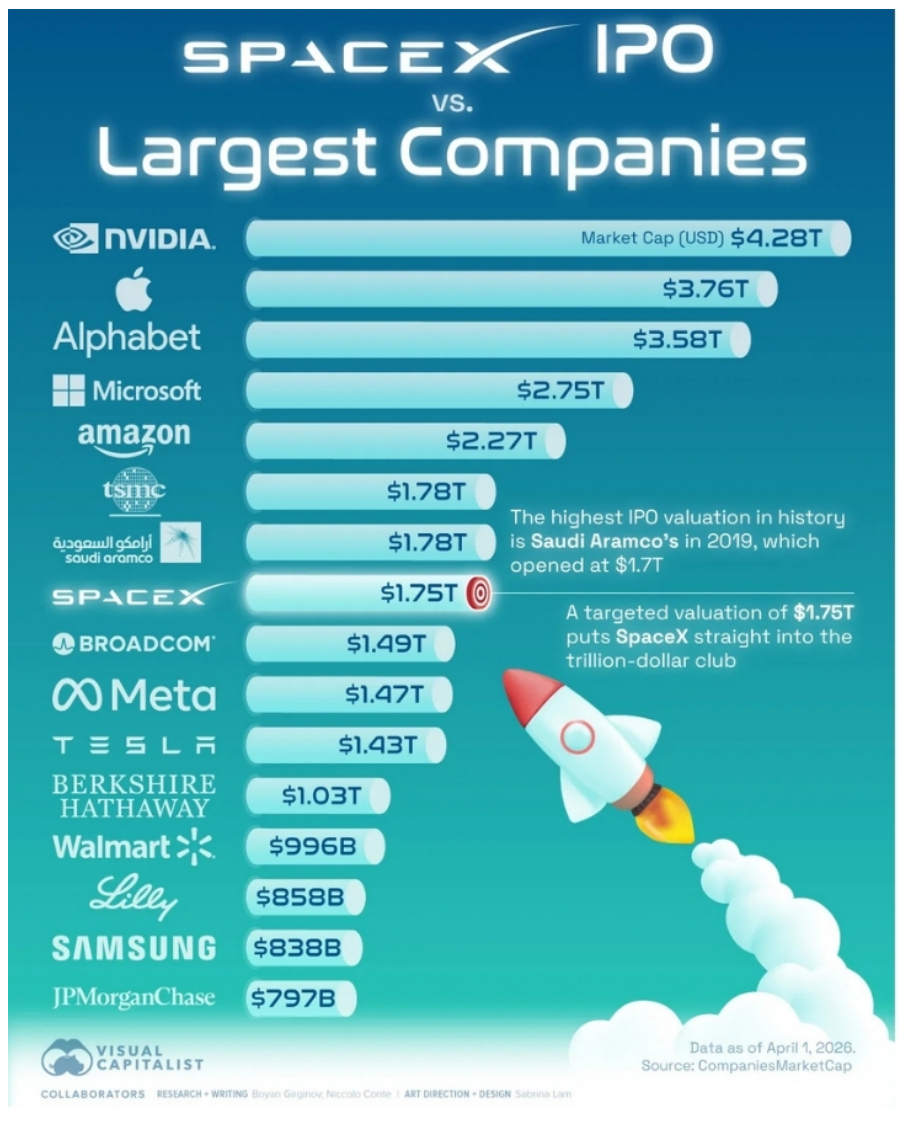

The mechanics are straightforward. Once a newly listed company becomes large enough to qualify for a major index, funds that track that index are required to buy it. In this instance, SpaceX is pushing to change the listing rules so that they are included in the indices quicker. Why else push for that, other than to maximise the pool of capital to support the share price? Index funds cannot wait for a better price or decide that the valuation looks too demanding or even decide to avoid what looks like a poor company. Their role is simply to mirror the index constituents.

For investors, the key point is that passive funds become buyers because the index says so, not because someone has assessed whether the shares represent compelling value at that particular price.

SpaceX illustrates what buying at that point in the process can imply for investors. At the expected IPO valuation, it would list at a price-to-sales multiple around 40 times more expensive than the average S&P 500 company. Expectations are high.

For investors to earn attractive long-term returns from that starting point, revenues would need to grow rapidly for many years, market enthusiasm for the company’s prospects would need to persist, and the business would need to execute its plan well. That is not impossible, but it does require a fairly specific future to unfold, one that many investors may not realise they are implicitly relying on when they buy a low-cost index fund.

How this differs from active investing

Active managers have more flexibility. They can invest earlier, later, or not at all. Some have owned businesses like SpaceX for years through private markets, at far lower valuations than those implied today. For example, several investment funds which can hold private assets, such as Scottish Mortgage Investment Trust (a UK-listed investment trust managed by Baillie Gifford), built their SpaceX position when the company was valued at roughly a twentieth of today's implied price. Others may wait for the post-IPO hype to die down, with hopefully a better entry point.

Passive funds have not had access to these opportunities for a long time, given the popularity of companies remaining private for longer. SpaceX is coming to market after 26 years as a private company, where the average time to reach this milestone is usually less than half this time.

This is not an argument for active over passive investing. It is an argument for understanding what passive does and does not offer. Over the past decade, strong market returns and steady inflows into index funds have reinforced each other. Prices rose, index weights increased, and more money followed by default. That process can also work in reverse. Investors and advisers who have only experienced the rising side of that cycle should be mindful that the same forces can amplify declines when sentiment changes.

What this means for investors

Broad, diversified, low-cost passive exposure remains sensible for most portfolios. But passive has never meant "risk-free" or "valuation-agnostic". It means owning the market at the price the market sets. In 2026, that price already reflects considerable optimism about the future, and with the new cohort of listings, that optimism is set to be tested even further. With heightened levels of company concentration in these indices, the foundation of passive investing – broad diversification – is being undermined. Investors need to be conscious of this exposure when assessing their investment strategies.

[1] A throwback to the dotcom bubble, many companies IPOd but with little in the way of earnings, assets or even a proven business model. Needless to say, it didn’t end well for investors.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Any potential listings, valuations and timings discussed are subject to change.

Comments