From Prime to Repo: A Cleaner Benchmark for a Lower-Rate South Africa

- bespoke62

- Mar 11

- 5 min read

Most people know their loan is priced at “Prime plus or minus a percentage”. But what exactly is Prime? Prime is the standard interest rate banks use as a starting point when pricing home loans, car finance and personal loans. Your actual rate is then adjusted up or down from that base, depending on your risk profile.

Prime is linked to the repo rate, the rate set by the South African Reserve Bank (SARB). Since 2001, Prime has been set at 3.5% above repo. This structure allows changes in the Reserve Bank’s policy rate to flow through directly to the rates banks charge and helps keep loan pricing consistent across institutions.

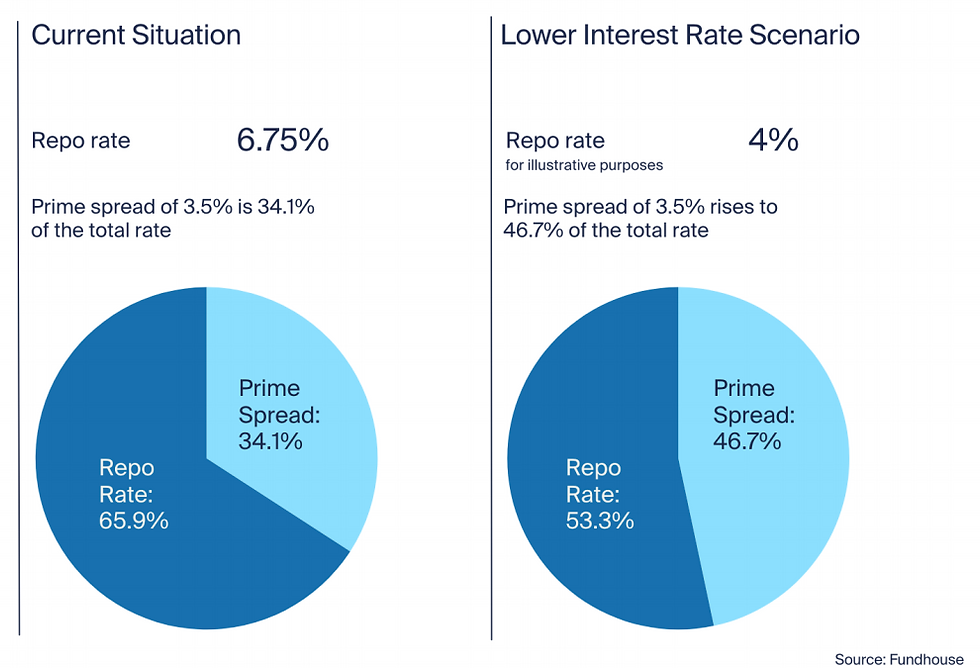

The chart below shows the constant Prime spread of 3.5% to the repo rate.

The 3.5% difference wasn’t arbitrary. It reflected how banks funded themselves at the time and created a predictable benchmark that reduced the old practice of banks adjusting their own base rates independently.

However, while the framework worked well when introduced, the economy and financial system have evolved. Inflation dynamics, funding markets and the broader operating environment have shifted.

Today, with the repo rate at 6.75% and Prime at 10.25%, the same 3.5% spread remains in place.

Why transparency is front and centre now

Transparency is the practical lever. It allows borrowers to see what they are paying for and understand why quotes differ.

SARB Governor Lesetja Kganyago has openly signalled that the “most natural outcome would be that we just get rid of Prime”, arguing the central bank wants more transparency so consumers can understand what they are actually paying for.

The SARB has formally reviewed the Prime benchmark, acknowledging that while Prime is widely understood, it may obscure the real building blocks of a customer’s rate, such as bank funding costs, the borrower’s risk, capital requirements, and competitive pressures.

Analysts and industry bodies caution that changing the benchmark alone won’t automatically lower borrowing costs, because the adjustments to Prime reflect the borrower’s risk profile and loan structure.

Keeping a simple label like “Prime” helped people compare quotes, but it can also mask what’s in the price. A modernised system as proposed by the SARB could show the components, repo + bank funding margin + risk margin + fees, more explicitly.

The case for changing how Prime is calculated (or scrapping it)

The 3.5% spread is a 2001 relic

It ensured that banks implemented changes to the repo quickly and effectively to change lending conditions in the economy, but financial markets, funding structures and regulation have moved on.

A fixed spread can become too blunt as the economy shifts to a long-term lower-inflation and interest-rate environment.

When interest rates move lower, the fixed 3.5% gap between repo and Prime doesn’t adjust with them. As a result, this unchanging portion makes up a larger share of the total rate. At a repo rate of 6.75%, the 3.5% spread is roughly a third of Prime; if repo falls to 4%, that same spread becomes almost half.

This is the core issue: as rates decline, the fixed spread absorbs more of the total, meaning borrowers see a smaller benefit from repo cuts. In a lower rate environment, the Prime structure becomes increasingly restrictive, which is why the SARB is reconsidering whether a fixed 3.5% premium still serves the system well.

Transparency and accountability

Regulators want consumers to see the components of their interest rate rather than a single benchmark plus/minus, which can hide how the bank has priced the loan.

Aligning with global best practice

Many developed markets, such as Germany and the UK, price loans off the official central bank policy rate or transparent market-based rates plus clearly disclosed margins.

Avoiding false expectations

Because Prime is widely quoted, it can create the impression that it is the “standard” rate everyone should receive. In reality, most borrowers pay Prime plus because of their individual risk profile. A cleaner framework could set expectations correctly and improve comparison shopping.

Consistency with a new inflation regime

With the SARB signalling a preference for a lower inflation anchor of 3%, with a tolerance range of 1% either way, a fixed 3.5% wedge may be out of step with a lower inflation, lower interest-rate environment.

If Prime goes away, what replaces it?

If the label changes, the logic should not: the interest rate still reflects policy, funding costs, borrower risk and fees, only now it is visible.

The most likely replacement is a “SARB Policy Rate (SPR)/repo + margin” convention, with banks disclosing the pieces of that margin (funding, risk, capital). Some variation by bank is expected, but the maths becomes clearer for borrowers. Other possibilities include redefining the Prime formula or governing it more explicitly.

Crucially, the banking industry notes that borrowers shouldn’t expect automatic savings simply because the label changes. The cost of loans is anchored in banks’ costs and risk, not the existence of Prime.

What happens to existing Prime-linked contracts?

According to the SARB, more than 12 million credit agreements, worth over R3.2 trillion, are currently linked to Prime. These contracts cannot simply be rewritten. To manage the transition, the SARB proposes using a fallback spread of 3.5% above the SPR to replace Prime in existing agreements.

This ensures that if the reference rate shifts from Prime to SPR, borrowers do not see unexpected changes in their interest costs, keeping pricing stable and providing a smooth transition into the new SPR-based benchmark system.

An optimistic but realistic path to lower rates for ordinary South Africans

Reform is the enabler, not the discount. Here is how transparency can translate into better pricing over time.

Transparent, line-by-line quotes

Banks quote SPR + funding margin + risk margin + fees, rather than “Prime ± x%.” Borrowers can compare offers line by line and increase competitive pressure.

Increased competition, especially from new digital-only lenders/banks

With clearer like-for-like comparisons, low-cost funders (or digital banks) can undercut incumbents on the funding margins.

More accurate risk-based pricing

When risk margins are visible, stronger borrowers can challenge high pricing or switch lenders if the margin looks out of line relative to their score. Banks respond with finer-grained pricing, rewarding good credit histories more aggressively, nudging average rates down, especially for safer borrowers.

Macro tailwinds amplify the effect

If the SARB achieves a durably lower inflation trajectory under its tighter target, the SPR and market funding costs tend to settle lower. A transparent benchmark passes those gains on more cleanly to consumers, instead of being muted by a fixed legacy spread.

Net result in the optimistic case

Transparency, competition and lower inflation can reduce average borrowing costs over time. The effect is gradual, not an overnight windfall, but it does add up to meaningful savings for long-term borrowers with solid credit records.

The structural shift that matters

The opportunity is structural: a benchmark that fits a lower inflation economy and passes improvements through more fairly.

What matters more is the transition to a modern, transparent, risk-sensitive framework. South Africa is shifting into a lower-inflation, lower interest-rate environment, which makes a fixed 3.5% Prime premium less appropriate. Reforming Prime is a necessary step if households and businesses are to benefit fully from a new economic regime.

If the benchmark review results in a more modern and transparent system, the country could see:

Low borrowing costs (over time)

Stronger economic activity

An economy that works better for households and businesses

That’s the real opportunity, not a quick Prime cut, but a cleaner system that supports long-term growth.

[1] The regulatory buffers banks must hold that affect how they price loans.

Comments